Supply and Demand

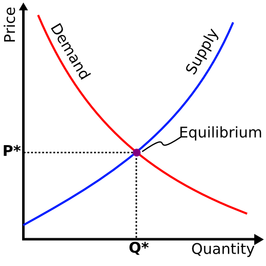

Demand refers to the quantity of a good that is desired by buyers. An important distinction to make is the difference between demand and the quantity demanded. The quantity demanded refers to the specific amount of that product that buyers are willing to buy at a given price. This relationship between price and the quantity of product demanded at that price is defined as the demand relationship.

Factors Affecting Demand

1. Substitutes

2. Diminishing Marginal Utility

3. Weather/Seasons

4. Change in Income

5. Number of Buyers

6. Styles, Tastes and Habits

Supply is defined as the total quantity of a product or service that the marketplace can offer. The quantity supplied is the amount of a product/service that suppliers are willing to supply at a given price. This relationship between price and the amount of a good/service supplied is known as the supply relationship.

Factors Affecting Supply

1. Cost of Production

2. Number of Sellers/Producers

At equilibrium, the quantity supplied and quantity demanded intersect and are equal. At equilibrium price, suppliers are selling all the goods that they have produced and consumers are getting all the goods that they are demanding. This is the optimal economic condition, where both consumers and producers of goods and services are satisfied.

Demand refers to the quantity of a good that is desired by buyers. An important distinction to make is the difference between demand and the quantity demanded. The quantity demanded refers to the specific amount of that product that buyers are willing to buy at a given price. This relationship between price and the quantity of product demanded at that price is defined as the demand relationship.

Factors Affecting Demand

1. Substitutes

2. Diminishing Marginal Utility

3. Weather/Seasons

4. Change in Income

5. Number of Buyers

6. Styles, Tastes and Habits

Supply is defined as the total quantity of a product or service that the marketplace can offer. The quantity supplied is the amount of a product/service that suppliers are willing to supply at a given price. This relationship between price and the amount of a good/service supplied is known as the supply relationship.

Factors Affecting Supply

1. Cost of Production

2. Number of Sellers/Producers

At equilibrium, the quantity supplied and quantity demanded intersect and are equal. At equilibrium price, suppliers are selling all the goods that they have produced and consumers are getting all the goods that they are demanding. This is the optimal economic condition, where both consumers and producers of goods and services are satisfied.

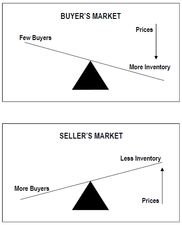

Buyer's Market is the best time for consumers to buy. A relatively small demand and large supply of a good or service have resulted in low prices.

Seller's Market is when the quantity demanded is much greater than the quantity supplied, resulting in higher prices. Consumers will buy regardless of high prices.

Elasticity

The degree to which a demand or supply curve reacts to a change in price is the curve's elasticity. Elasticity varies among products because some products may be more essential to the consumer. Products that are necessities are more insensitive to price changes because consumers would continue buying these products despite price increases. Conversely, a price increase of a good or service that is considered less of a necessity will deter more consumers because the opportunity cost of buying the product will become too high.

A good or service is considered to be highly elastic if a slight change in price leads to a sharp change in the quantity demanded or supplied. Usually these kinds of products are readily available in the market and a person may not necessarily need them in his or her daily life. On the other hand, an inelastic good or service is one in which changes in price witness only modest changes in the quantity demanded or supplied, if any at all. These goods tend to be things that are more of a necessity to the consumer in his or her daily life.

The degree to which a demand or supply curve reacts to a change in price is the curve's elasticity. Elasticity varies among products because some products may be more essential to the consumer. Products that are necessities are more insensitive to price changes because consumers would continue buying these products despite price increases. Conversely, a price increase of a good or service that is considered less of a necessity will deter more consumers because the opportunity cost of buying the product will become too high.

A good or service is considered to be highly elastic if a slight change in price leads to a sharp change in the quantity demanded or supplied. Usually these kinds of products are readily available in the market and a person may not necessarily need them in his or her daily life. On the other hand, an inelastic good or service is one in which changes in price witness only modest changes in the quantity demanded or supplied, if any at all. These goods tend to be things that are more of a necessity to the consumer in his or her daily life.

Gross National Product (GNP)

As defined, the GNP is the final, total value of all goods and services produced by a country in a single year. It measures the health of an economy.

GNP = C + I + F + G

C = Personal Consumption

I = Gross Private Domestic Investment

F = Net Exports to Foreign Nations

G = Government Purchases

The difference between GNP and GDP?

Gross Domestic Product (GDP) is the measure economists typically use to indicate the total size or value of economic production in an economy. There is a similar measure called Gross National Product (GNP).

So what’s the difference? Well, first let’s look at the similarities. Both GDP and GNP measure “the market value of all goods and services produced for final sale in an economy”. The difference is in how we define “the economy”. GDP focuses on domestic production. In other words, it defines a nation’s economy in geographical terms. Whatever is actually produced inside the country, regardless of who is doing the producing or who owns the productive capital that produces it. In the case of the U.S., it means whatever is produced within the 50 states. GNP however focuses on the production by nationals. In other words, GNP defines the nation’s economy in people or resident terms. It counts whatever is produced by the residents or citizens of a nation regardless of where those people may be doing the producing. In the case of the U.S., this means that GNP measures anything produced by Americans or American-owned capital wherever it may be in the world.

So in practical terms it’s multinational corporations where the differences arise. Let’s consider the auto industry. If Ford, a U.S. company, produces in cars in Dearborn, MI, then the value of the cars counts toward both GDP and GNP. Similarly, when BMW, a German corporation, builds cars in Germany, it counts towards both German GDP and GNP. But when Ford produces cars in Cologne, Germany, it counts toward U.S. GNP (Ford is American producing in Germany) but not toward US GDP. Instead Ford production in Cologne counts towards German GDP since it is geographically produced in Germany. Likewise, BMW production in Alabama in the States counts toward US GDP and German GNP, but not German GDP.

As defined, the GNP is the final, total value of all goods and services produced by a country in a single year. It measures the health of an economy.

GNP = C + I + F + G

C = Personal Consumption

I = Gross Private Domestic Investment

F = Net Exports to Foreign Nations

G = Government Purchases

The difference between GNP and GDP?

Gross Domestic Product (GDP) is the measure economists typically use to indicate the total size or value of economic production in an economy. There is a similar measure called Gross National Product (GNP).

So what’s the difference? Well, first let’s look at the similarities. Both GDP and GNP measure “the market value of all goods and services produced for final sale in an economy”. The difference is in how we define “the economy”. GDP focuses on domestic production. In other words, it defines a nation’s economy in geographical terms. Whatever is actually produced inside the country, regardless of who is doing the producing or who owns the productive capital that produces it. In the case of the U.S., it means whatever is produced within the 50 states. GNP however focuses on the production by nationals. In other words, GNP defines the nation’s economy in people or resident terms. It counts whatever is produced by the residents or citizens of a nation regardless of where those people may be doing the producing. In the case of the U.S., this means that GNP measures anything produced by Americans or American-owned capital wherever it may be in the world.

So in practical terms it’s multinational corporations where the differences arise. Let’s consider the auto industry. If Ford, a U.S. company, produces in cars in Dearborn, MI, then the value of the cars counts toward both GDP and GNP. Similarly, when BMW, a German corporation, builds cars in Germany, it counts towards both German GDP and GNP. But when Ford produces cars in Cologne, Germany, it counts toward U.S. GNP (Ford is American producing in Germany) but not toward US GDP. Instead Ford production in Cologne counts towards German GDP since it is geographically produced in Germany. Likewise, BMW production in Alabama in the States counts toward US GDP and German GNP, but not German GDP.

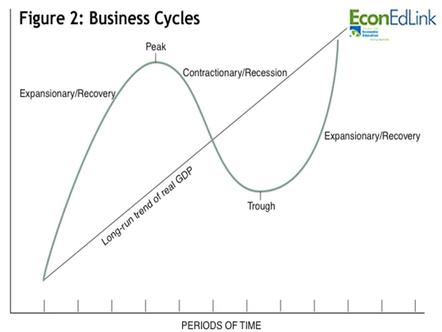

Business Cycles

A predictable long-term pattern of alternating periods of economic growth (recovery) and decline (recession), characterized by changing employment, industrial productivity, and interest rates. also called economic cycle. Read more: http://www.investorwords.com/625/business_cycle.html#ixzz2jiQIb0ot

A business cycle is identified as a sequence of four phases:

A predictable long-term pattern of alternating periods of economic growth (recovery) and decline (recession), characterized by changing employment, industrial productivity, and interest rates. also called economic cycle. Read more: http://www.investorwords.com/625/business_cycle.html#ixzz2jiQIb0ot

A business cycle is identified as a sequence of four phases:

- Contraction: A slowdown in the pace of economic activity

- Trough: The stage of the economy's business cycle that marks the end of a period of declining business activity and the transition to expansion.

- The lower turning point of a business cycle, where a contraction turns into an expansion

- Expansion: A speedup in the pace of economic activity

- Peak: The upper turning of a business cycle