Profit Motive

A profit motive is, quite simply, the goal of most businesses, to make a profit or have more money coming into the business than is spent by the business. In capitalism, it is generally considered to be the main reason most businesses exist and is closely tied to the concept of “self-interest.” It has also developed a fairly poor reputation and is considered by many to be one of the primary reasons that businesses or corporations are not trusted or require regulation. A profit motive, ultimately, should be devoid of morality, and the choices made by others in pursuit of higher profits should typically be considered rather than the desire for profit itself. from http://www.wisegeek.com/what-is-a-profit-motive.htm

Profit Defined

The reward for doing business.

Elements of the Income Statement

An Income Statement is a standard financial document that summarizes a company's revenue and expenses for a specific period of time. It is important that both investors and company managers be able to read and understand this document in order to understand the company's financial health.

Sales Revenue: all the money received from doing business

Cost of Goods Sold: it is usually the largest expense on the income statement of a company selling products or goods.

Gross Profit: is calculated by subtracting the total cost of goods sold from the total sales revenue. Gross profit is

essential in calculating the gross margin (gross profit divided by sales), which measures efficiency. It's important to have a strong gross margin percentage and to track percentage gains and losses to spot negative trends before the business gets into financial trouble.

Operating Expenses: expenditure that a business incurs as a result of performing its normal business operations.

Net Profit: Often referred to as the bottom line, net profit is calculated by subtracting a company's total expenses from total revenue, thus showing what the company has earned (or lost) in a given period of time (usually one year). also called net income or net earnings.

Cost of Goods Sold: it is usually the largest expense on the income statement of a company selling products or goods.

Gross Profit: is calculated by subtracting the total cost of goods sold from the total sales revenue. Gross profit is

essential in calculating the gross margin (gross profit divided by sales), which measures efficiency. It's important to have a strong gross margin percentage and to track percentage gains and losses to spot negative trends before the business gets into financial trouble.

Operating Expenses: expenditure that a business incurs as a result of performing its normal business operations.

Net Profit: Often referred to as the bottom line, net profit is calculated by subtracting a company's total expenses from total revenue, thus showing what the company has earned (or lost) in a given period of time (usually one year). also called net income or net earnings.

Microeconomics versus Macroeconomics

In our marketing class we focus on Microeconomics and our social studies department focuses on Macroeconomics.

Micro economics is concerned with:

In our marketing class we focus on Microeconomics and our social studies department focuses on Macroeconomics.

- Microeconomics is the study of particular markets, and segments of the economy. It looks at issues such as consumer behavior, individual labor markets, and the theory of firms.

- Macroeconomics is the study of the whole economy. It looks at ‘aggregate’ variables, such as aggregate demand, national output and inflation.

Micro economics is concerned with:

- Supply and demand in individual markets

- Individual consumer behavior.

- Individual labor markets – e.g. demand for labor

- Competition in the marketplace

- Monetary / fiscal policy. e.g. what effect does interest rates have on whole economy?

- Reasons for inflation, and unemployment

- Economic Growth

- International trade and globalization

- Reasons for differences in living standards and economic growth between countries.

- Government borrowing

The Three Limited Resources/Factors of Productions

Land: Land includes all natural physical resources.

Labor: Labor is the human input into production.

Capital: Capital goods are used to produce other consumer goods and services in the future.

Fixed capital includes machinery, equipment, new technology, factories and other building.

Working capital means stocks of finished and semi-finished goods (or components) that will be either consumed in the near future or will be made into consumer goods.

Labor: Labor is the human input into production.

Capital: Capital goods are used to produce other consumer goods and services in the future.

Fixed capital includes machinery, equipment, new technology, factories and other building.

Working capital means stocks of finished and semi-finished goods (or components) that will be either consumed in the near future or will be made into consumer goods.

Economic Objective

The economic objective is to get the most with the least. We are all looking for ways to stretch a dollar. How can we get the most (benefit) from our limited resource (this dollar).

The economic objective is to get the most with the least. We are all looking for ways to stretch a dollar. How can we get the most (benefit) from our limited resource (this dollar).

Three Basic Economic Questions

Every economy needs to answer the three basic economic questions:

1. What to produce?

2. How to produce it?

3. Who gets it?

Every economy needs to answer the three basic economic questions:

1. What to produce?

2. How to produce it?

3. Who gets it?

Opportunity Cost

Simply stated, an opportunity cost is the cost of a missed opportunity. It is the opposite of the benefit that would have been gained had an action, not taken, been taken—the missed opportunity. This is a concept used in economics. Applied to a business decision, the opportunity cost might refer to the profit a company could have earned from its capital, equipment, and real estate if these assets had been used in a different way. The concept of opportunity cost may be applied to many different situations. It should be considered whenever circumstances are such that scarcity necessitates the election of one option over another. Opportunity cost is usually defined in terms of money, but it may also be considered in terms of time, person-hours, mechanical output, or any other finite resource. Defined from: http://www.inc.com/encyclopedia/opportunity-cost.html

Trade Offs

When we sacrifice one thing to obtain another, that's called a trade-off. Only have enough cash to buy a bike or a snowboard, but not both? That's a trade-off. Trying to decide whether to take the Fourth of July off to spend with your family, or to go to work and make extra overtime? That's a trade-off. Trade-offs create opportunity costs, one of the most important concepts in economics. Whenever you make a trade-off, the thing that you do not choose is your opportunity cost. To butcher the poet Robert Frost, opportunity cost is the path not taken (and that makes all the difference). You bought that bike? Then the snowboard was your opportunity cost. Decided to work on the Fourth of July? Your opportunity cost was a relaxing day hanging out with the family at the BBQ.

Everything has opportunity costs. If you just bought something, you could have always chosen to buy something else instead. If you just chose to spend your time in a particular way, you could have always done something else. "Something else" is your opportunity cost. Defined from: http://www.shmoop.com/economic-principles/opportunity-costs.html

Simply stated, an opportunity cost is the cost of a missed opportunity. It is the opposite of the benefit that would have been gained had an action, not taken, been taken—the missed opportunity. This is a concept used in economics. Applied to a business decision, the opportunity cost might refer to the profit a company could have earned from its capital, equipment, and real estate if these assets had been used in a different way. The concept of opportunity cost may be applied to many different situations. It should be considered whenever circumstances are such that scarcity necessitates the election of one option over another. Opportunity cost is usually defined in terms of money, but it may also be considered in terms of time, person-hours, mechanical output, or any other finite resource. Defined from: http://www.inc.com/encyclopedia/opportunity-cost.html

Trade Offs

When we sacrifice one thing to obtain another, that's called a trade-off. Only have enough cash to buy a bike or a snowboard, but not both? That's a trade-off. Trying to decide whether to take the Fourth of July off to spend with your family, or to go to work and make extra overtime? That's a trade-off. Trade-offs create opportunity costs, one of the most important concepts in economics. Whenever you make a trade-off, the thing that you do not choose is your opportunity cost. To butcher the poet Robert Frost, opportunity cost is the path not taken (and that makes all the difference). You bought that bike? Then the snowboard was your opportunity cost. Decided to work on the Fourth of July? Your opportunity cost was a relaxing day hanging out with the family at the BBQ.

Everything has opportunity costs. If you just bought something, you could have always chosen to buy something else instead. If you just chose to spend your time in a particular way, you could have always done something else. "Something else" is your opportunity cost. Defined from: http://www.shmoop.com/economic-principles/opportunity-costs.html

Economic Utility

Utility means usefulness. How can you make something useful for your customer?

There are five utilities:

1. Form; when you add to raw materials. Taking lemons, water and sugar and mixing the elements together makes lemonade. This makes the raw materials more useful.

2. Time; when you are available to sell. A lemonade stand should be open on hot, sunny days.

3. Place; where you sell. A lemonade stand should be open on a business sidewalk or park.

4. Possession; helping your customers own the product/service. A jogger stops at your lemonade stand and doesn't have their wallet with them. You extend credit to the jogger. This is helping them own that glass of lemonade.

5. Information; providing information to the market about your product/service.

Form utility has nothing to do with Marketing because Marketing gets the product from the producer to the consumer. Marketers do not make the product. Form utility is all about making something.

Utility means usefulness. How can you make something useful for your customer?

There are five utilities:

1. Form; when you add to raw materials. Taking lemons, water and sugar and mixing the elements together makes lemonade. This makes the raw materials more useful.

2. Time; when you are available to sell. A lemonade stand should be open on hot, sunny days.

3. Place; where you sell. A lemonade stand should be open on a business sidewalk or park.

4. Possession; helping your customers own the product/service. A jogger stops at your lemonade stand and doesn't have their wallet with them. You extend credit to the jogger. This is helping them own that glass of lemonade.

5. Information; providing information to the market about your product/service.

Form utility has nothing to do with Marketing because Marketing gets the product from the producer to the consumer. Marketers do not make the product. Form utility is all about making something.

TYPES OF ECONOMIC SYSTEMS

Traditional System

A pure traditional economy answers the basic economic questions according to tradition. Things are done as they were in the past based on tradition, customs, and beliefs (religious).

Examples: Certain areas in developing countries

Command System

The individual has little influence over how the economic questions are answered in a pure command system. The government controls the factors of production and makes all decisions. This could be one person, a small group, or central planners who decide what resources to use at each step of production and the distribution of goods and

services. The government even decides the role everyone will play. It guides people into certain jobs.

Examples: North Korea, Cuba

Market or Capitalist System

Capitalism is a pure market economy. In this system the government does not intervene. Individuals own the factors of production and they decide the answers of the basic economic questions. The market is the freely chosen activities between buyers and sellers of goods and services.

Examples: the underground economy, 19th century Britain

Mixed Economic System:

Many economists doubt that “pure” economic systems ever existed. A mixed economic system contains elements of the market and command systems, with elements of traditional as well. For example, there is some private ownership in the Peoples’ Republic of China. Some private ownership also existed in the former Soviet Union.

Examples: United States, most other nations

Traditional System

A pure traditional economy answers the basic economic questions according to tradition. Things are done as they were in the past based on tradition, customs, and beliefs (religious).

Examples: Certain areas in developing countries

Command System

The individual has little influence over how the economic questions are answered in a pure command system. The government controls the factors of production and makes all decisions. This could be one person, a small group, or central planners who decide what resources to use at each step of production and the distribution of goods and

services. The government even decides the role everyone will play. It guides people into certain jobs.

Examples: North Korea, Cuba

Market or Capitalist System

Capitalism is a pure market economy. In this system the government does not intervene. Individuals own the factors of production and they decide the answers of the basic economic questions. The market is the freely chosen activities between buyers and sellers of goods and services.

Examples: the underground economy, 19th century Britain

Mixed Economic System:

Many economists doubt that “pure” economic systems ever existed. A mixed economic system contains elements of the market and command systems, with elements of traditional as well. For example, there is some private ownership in the Peoples’ Republic of China. Some private ownership also existed in the former Soviet Union.

Examples: United States, most other nations

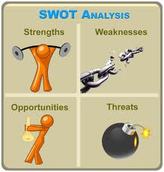

SWOT Analysis

The name says it: Strength, Weakness, Opportunity, Threat. A SWOT analysis guides you to identify the positives and negatives inside your organization (S-W) and outside of it, in the external environment (O-T). Developing a full awareness of your situation can help with both strategic planning and decision-making.

The SWOT method was originally developed for business and industry, but it is equally useful in the work of community health and development, education, and even personal growth.

SWOT is not the only assessment technique you can use, but is one with a long track record of effectiveness. SWOT essentially tells you what is good and bad about a business or a particular proposition. If it's a business, and the aim is to improve it, then work on translating:

The name says it: Strength, Weakness, Opportunity, Threat. A SWOT analysis guides you to identify the positives and negatives inside your organization (S-W) and outside of it, in the external environment (O-T). Developing a full awareness of your situation can help with both strategic planning and decision-making.

The SWOT method was originally developed for business and industry, but it is equally useful in the work of community health and development, education, and even personal growth.

SWOT is not the only assessment technique you can use, but is one with a long track record of effectiveness. SWOT essentially tells you what is good and bad about a business or a particular proposition. If it's a business, and the aim is to improve it, then work on translating:

- strengths (maintain, build and leverage),

- opportunities (prioritize and optimize),

- weaknesses (remedy or exit),

- threats (counter)

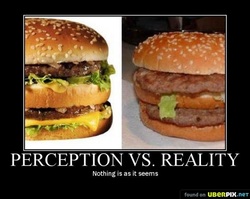

Perception Is Reality.

What your prospects, clients or customers perceive about you, your place of business and your level of success in business is imminently more important that what may be a different reality. For example, if you are a client of a high-end restaurant, and when you are in the restroom you notice that things are dirty, there are paper towels on the floor or something else unpleasant, it might be the last time you ever visit the location, even if the food is fabulous.

I once read a story about an airline executive who figured out that dirty tray tables led people to have less confidence in the airline and seek other providers. They’re thought process, “Well, if they can’t even clean the tray tables, what else aren’t they maintaining…I may not be safe on this airline…” Not the ideal thought process you want your clients to be experiencing as they start a trip with your company.

Websites are actually a very good example of this…if you are a large established company, but your website is difficult to use or amateurish people’s impression of you who choose to find you on the web, either before becoming a customer or after, may change dramatically. If you are a small company, even if you are just starting out, and you take the time to create a well thought out website, even if it is simple, it can change a lot about the way people perceive your business, making people think you are larger and more successful than you may actually be, helping them to have more confidence in you and your product or service.

What can you do to ‘clean up your act’ or add substance to your appearance? source: http://www.paysoncooper.com/101-marketing-strategies/in-marketing-perception-is-reality/

What your prospects, clients or customers perceive about you, your place of business and your level of success in business is imminently more important that what may be a different reality. For example, if you are a client of a high-end restaurant, and when you are in the restroom you notice that things are dirty, there are paper towels on the floor or something else unpleasant, it might be the last time you ever visit the location, even if the food is fabulous.

I once read a story about an airline executive who figured out that dirty tray tables led people to have less confidence in the airline and seek other providers. They’re thought process, “Well, if they can’t even clean the tray tables, what else aren’t they maintaining…I may not be safe on this airline…” Not the ideal thought process you want your clients to be experiencing as they start a trip with your company.

Websites are actually a very good example of this…if you are a large established company, but your website is difficult to use or amateurish people’s impression of you who choose to find you on the web, either before becoming a customer or after, may change dramatically. If you are a small company, even if you are just starting out, and you take the time to create a well thought out website, even if it is simple, it can change a lot about the way people perceive your business, making people think you are larger and more successful than you may actually be, helping them to have more confidence in you and your product or service.

What can you do to ‘clean up your act’ or add substance to your appearance? source: http://www.paysoncooper.com/101-marketing-strategies/in-marketing-perception-is-reality/